Quick Answer: The employer credit for family and medical leave provides small businesses a federal tax credit worth 12.5% to 25% of qualified leave costs. In 2026, you can claim this credit on actual wages paid during FMLA leave or on commercial insurance premiums. Qualification requires a written policy offering at least 50% pay to employees earning $96,000 or less.

Key Takeaways

- The Section 45S Paid Family and Medical Leave tax credit is now a permanent federal incentive for small businesses under the One Big Beautiful Bill Act (OBBBA).

- Eligible employers can secure a federal tax credit ranging from 12.5% to 25% to directly offset the costs of providing qualified leave to their team.

- Starting in 2026, businesses can claim this credit against commercial insurance premiums (like group short-term disability policies) even if no employees actually take leave during the year.

- To qualify for the credit, an employee must work at least 20 hours per week and have earned a prior-year compensation of $96,000 or less.

- To lock in these savings, your Indianapolis business must establish a formal, written employee policy that explicitly guarantees a minimum of two weeks of FMLA-qualifying leave at 50% wage replacement or higher.

When life happens to your employees (whether it’s the birth of a child, a medical emergency, or a sudden family crisis), you have to figure out the logistical reality for your Marion County business:

How will your cash flow sustain paying a regular salary to an employee who isn’t actively working?

That’s where the Section 45S tax credit can help: an incentive that provides a dollar-for-dollar tax credit to offset up to 25% of those leave costs.

And thanks to recent permanent updates under the OBBBA, the credit now offers more value for small businesses than ever.

If you want to protect your bottom line while still taking amazing care of your team, it’s time to consider how this credit fits into your tax strategy.

What is the Section 45S tax credit?

The Section 45S tax credit, or the employer credit for family and medical leave, is a federal tax incentive designed to help small business owners offset the costs of providing paid family and medical leave to their team. The credit amount is based on a percentage of the wages you continue to pay employees while they’re out on qualified leave. It was recently made permanent by the OBBBA.

The point of this credit is to support your bottom line when your employees need time off for major life events. Like the birth or adoption of a child, caring for an immediate family member with a severe illness, dealing with their own serious health crisis, or managing military-related family emergencies.

How much is the employer credit for family and medical leave worth?

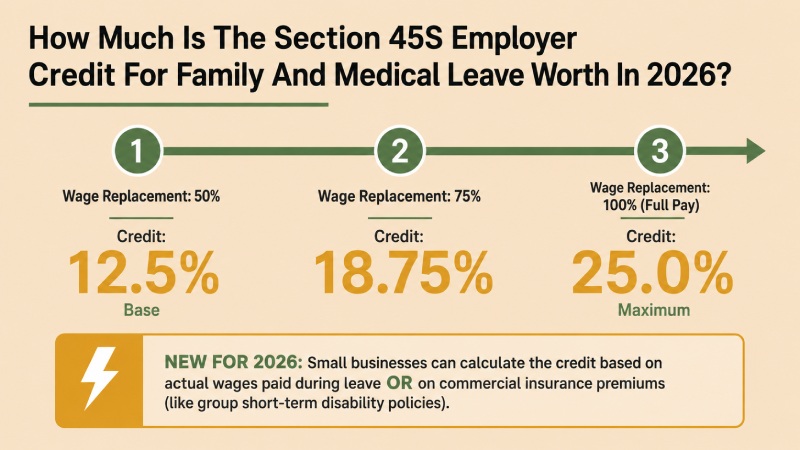

The credit ranges from 12.5% to 25% of the wages you pay during your employee’s leave, for up to 12 weeks per employee per tax year.

The exact percentage depends on how much of their normal salary you cover. If you pay 50% of the employee’s regular wages while they are on leave, you qualify for the base credit of 12.5%.

For every percentage point of pay you provide above the 50% threshold, the tax credit increases. If you choose to pay 100% of their regular wages during their leave, your credit hits the maximum of 25%.

Also, thanks to the OBBBA, you can now calculate the credit based on the commercial insurance premiums you pay to fund a qualifying leave policy (such as a short-term disability policy).

Who qualifies as an eligible employee?

To qualify, an employee must have been on your payroll for at least one year. Also, their compensation from the prior year can’t exceed a strict federal income threshold. For the 2026 tax year, the cap restricts the credit to employees who earned $96,000 or less in 2025.

How to write a paid leave policy

To be eligible for this credit, your Indianapolis business has to have a formal, written paid leave policy already in place that explicitly guarantees the following protections:

- The policy must offer at least two weeks of paid family and medical leave annually for full-time employees (and a prorated amount for part-time workers).

- The policy must guarantee at least 50% of the employee’s standard wages.

- The document must contain strict non-interference and anti-discrimination clauses, so employees won’t be penalized, demoted, or discouraged from using their leave.

Also, the paid leave must be specifically earmarked for Family and Medical Leave Act (FMLA) purposes.

For example: Sarah owns a boutique marketing agency and gives her team 4 weeks of “no-questions-asked” PTO to use for vacation, sick days, or personal time. One of her copywriters uses 3 weeks of this PTO bucket to undergo and recover from a major medical procedure.

Even though the employee used the time off for a genuine, FMLA-qualifying medical emergency, Sarah cannot claim the employer credit for family and medical leave on those wages. Because standard PTO or vacation buckets don’t count.

Under the OBBBA, your written policy only needs to cover employees who customarily work more than 20 hours per week, removing the logistical headache of tracking irregular part-time staff.

And while the standard rule requires an employee to be on your payroll for a full year, you can now elect to reduce this requirement to just six months.

The “no double-dipping” rule

If you choose to claim the Section 45S credit, you have to reduce your business’s standard deduction for employee wages by the exact amount of the credit you receive. And, the specific wages used to calculate your Section 45S credit can’t be used to qualify for any other federal general business tax credits.

Which means maintaining meticulous payroll records, tracking precise leave dates, and preserving your written policy documents are vital to surviving an IRS audit and maximizing your return.

If your state already mandates paid family and medical leave, the OBBBA clears up the double-dipping ambiguity: State-mandated benefits can count toward meeting the required baseline (e.g., offering 2 weeks of leave at 50% pay).

But state-mandated payments cannot be used to calculate the federal credit. You can only claim the credit on voluntary compensation paid above and beyond what the state forces you to pay.

Should you claim the employer credit for family and medical leave?

If you’re wondering if this credit could help lower your business’s tax liability, there are a few items we need to consider first:

1. Your employee compensation and hours distribution. We need to check your payroll data to see who actually qualifies. First, we need to calculate how many of your employees earned $96,000 or less in the prior year. (The bigger your middle-class or hourly workforce, the more potential savings to be had.)

Then, we’ll analyze how many part-time employees work more than 20 hours per week, because your written policy must uniformly cover them.

2. Your funding model. Do you want to pay wages out of pocket when someone goes on leave, or do you prefer a predictable monthly insurance expense? Because the tax code allows you to claim the credit against commercial insurance premiums (like group short-term disability), I can run a comparative analysis to see which model saves you more cash while minimizing risk.

3. Your geographic footprint. Where are your employees physically located? If you have team members in states with state-mandated paid family leave laws, we need to look at what the state forces you to provide and calculate the tax benefit of voluntarily adding an extra layer of employer-funded pay to trigger the federal credit.

4. Your entity structure and current tax liability. For pass-through entities (S-Corps, LLCs, Partnerships), the credit flows to your personal tax return. So, we’ll have to look at your personal tax bracket and overall liability to make sure you can actually use the credit this year.

Also, if your business is projecting a net loss, you won’t owe federal income tax. We can plan a carry-forward strategy, banking the credit to offset up to 20 years of future tax bills.

How can I claim the employer credit for family and medical leave?

If you want to bake Section 45S into your tax planning this year, focus on taking these proactive steps right now:

Step 1: Pull your prior-year payroll reports

Ask your payroll provider for a report showing every employee’s total compensation and average weekly hours. Isolate the employees who earned $96,000 or less. This gives me the exact data I need to calculate your maximum potential tax credit.

Step 2: Request an insurance assessment

Contact your commercial insurance broker and ask for quotes on a group short-term disability policy or a private paid family leave policy that covers FMLA-qualifying events. I’ll analyze these quotes to find the tax-credit yield on those monthly premiums.

Step 3: Update your employee handbook

Work with an HR professional or employment attorney to draft the formal, written policy language required by the IRS, complete with the mandatory “non-interference” and “anti-retaliation” clauses. The policy must be active and communicated to your team before you can claim a single dollar of the credit.

Final thoughts

If you’re feeling a bit of administrative hesitation with these rules, don’t let that stop you from saving valuable tax dollars. I’m here to help you through the process.

Just get your appointment on my calendar, and we’ll audit your payroll, structure your written policy, and maximize the tax savings your small business is entitled to.

www.helmscpa.com/book-an-appointment/

FAQs

“Do I qualify for the Section 45S credit if my business has fewer than 50 employees?”

There is no minimum company size requirement to claim the Section 45S credit. While the traditional federal Family and Medical Leave Act (FMLA) mandate only applies to businesses with 50 or more workers, any small business can voluntarily choose to offer a qualifying policy and claim this tax credit, even if you only have two or three employees.

“Can I still get the Section 45S tax credit if nobody takes time off this year?”

Thanks to the 2026 OBBBA updates, if you use the premium method, you can claim a tax credit on the commercial insurance premiums you pay (like group short-term disability) throughout the year. The credit is tied to the money you spent on the policy premiums, meaning you still get your tax break even if your team stays perfectly healthy and nobody takes a single day of leave all year.

“Can I use my standard, multi-purpose PTO or vacation bucket to claim this credit?”

The IRS explicitly states that generic PTO, standard sick leave, or regular vacation days do not count toward the Section 45S credit. To qualify for the tax incentive, your written policy must state that the paid leave is exclusively designated for FMLA-qualifying events (such as the birth of a child, serious illness, or military caregiving) and cannot be used for generic personal time off.

“Can I claim the Section 45S tax credit for my own family leave if I am the business owner?”

The Section 45S credit is strictly designed for qualifying employees on your payroll. Because of strict IRS rules regarding business ownership, self-employment structures, and the fact that a qualifying employee’s prior-year compensation cannot exceed the middle-class income cap ($96,000 for the 2026 tax year), small business owners themselves almost never qualify for the credit on their own leave.

“How much tax credit do I get if my insurance policy covers 60% of an employee’s normal wages?”

You will receive a 15% tax credit. The Section 45S credit operates on a sliding scale. The baseline credit is 12.5% if you cover the minimum 50% of an employee’s wages. For every single percentage point of wage replacement you provide above that 50% baseline, your tax credit increases by 0.25%. Since a 60% wage replacement policy is 10 percentage points over the baseline, you add an extra 2.5% to your credit rate, bringing your total tax credit to 15% of your paid premiums or wages.

“If my state already mandates paid family leave, can I still claim the federal Section 45S credit?”

Only on voluntary amounts you pay above the state mandate. Under the 2026 rules, you can use your state-mandated program to prove your Marion County business meets the minimum eligibility requirements to participate. However, you cannot claim the federal tax credit on the baseline dollars the state forces you to pay. You can only claim the Section 45S credit if you voluntarily top up your policy to provide a higher percentage of wage replacement than the state baseline requires.

“Do I lose the credit if my business has a net loss this year?”

No, you do not lose it. Because Section 45S is a non-refundable general business credit, it cannot reduce your federal tax liability below zero to give you a cash refund in a loss year. However, the IRS allows you to bank the unused credit and carry it forward for up to 20 years to offset your future profitable years, or carry it back 1 year to get a refund on taxes you previously paid.